-

Letter from Jeffrey A. Porter, CPA, Chair, AICPA Tax Executive Committee, to Max Baucus, Chairman, and Orrin G. Hatch, Ranking Member, Senate Committee on Finance; Dave Camp, Chairman, and Sander Levin, Ranking Member, House Committee on Ways & Means, Re: Request for Legislation Permitting Administrative Relief for Certain Late Lifetime Qualified Terminable Interest Property Elections and Certain Late Qualified Revocable Trust Elections.

Jeffrey A. Porter and American Institute of Certified Public Accountants. Tax Executive Committee

-

Letter from Jeffrey A. Porter, CPA, Chair, AICPA Tax Executive Committee, to Max Baucus, Chairman, and Orrin G. Hatch, Ranking Member, Senate Committee on Finance; Dave Camp, Chairman, and Sander W. Levin, Ranking Member, House Committee on Ways and Means; Re: Simplification and Technical Legislative Proposals.

Jeffrey A. Porter and American Institute of Certified Public Accountants. Tax Executive Committee

-

Letter from Jeffrey A. Porter, CPA, Chair, AICPA Tax Executive Committee, to Max Baucus, Chairman, and Orrin G. Hatch, Ranking Member, Senate Committee on Finance, Re: Next Steps on Tax Reform.

Jeffrey A. Porter and American Institute of Certified Public Accountants. Tax Executive Committee

-

Letter from Jeffrey A. Porter, CPA, Chair, AICPA Tax Executive Committee, to Max Baucus, Chairman, Senate Committee on Finance; Orrin G. Hatch, Ranking Member, Senate Committee on Finance; and Bill Nelson, United States, Senate, Re: Comments on the Identity Theft and Tax Fraud Prevention Act of 2013 and Recommendations on Efforts to Combat Identity Theft.

Jeffrey A. Porter and American Institute of Certified Public Accountants. Tax Executive Committee

-

Letter from Jeffrey A. Porter, CPA, Chair, AICPA Tax Executive Committee, to Steven Miller, Acting Commissioner, and William J. Wilkins, Chief Counsel, Internal Revenue Service, Re: Comments Related to Notice of Proposed Rulemaking Issued on Employer Shared Responsibility for Health Insurance Coverage.

Jeffrey A. Porter and American Institute of Certified Public Accountants. Tax Executive Committee

-

Letter from Jeffrey A. Porter, CPA, Chair, AICPA Tax Executive Committee, to Steven T. Miller, Acting Commissioner, and William J. Wilkins, Chief Counsel, Internal Revenue Service, Re: Notice 2012-65--Information for Discharges of Indebtedness.

Jeffrey A. Porter and American Institute of Certified Public Accountants. Tax Executive Committee

-

Letter From Jeffrey A. Porter, CPA, Chair, AICPA Tax Executive Committee, to Steven T. Miller, Acting Commissioner, Internal Revenue Service, and William J. Wilkins, Chief Counsel, Internal Revenue Service, Re: Form 1099-MISC, Miscellaneous Income--Filing Requirements for Taxpayers With Rental Real Estate.

Jeffrey A. Porter and American Institute of Certified Public Accountants. Tax Executive Committee

-

. by Jeffrey A. Porter and American Institute of Certified Public Accountants. Tax Executive Committee")

Letter from Jeffrey A. Porter, CPA, Chair, AICPA Tax Executive Committee, to Steven T. Miller, Acting Commissioner, Internal Revenue Service, Re: Availability of Application Process to Obtain Preparer Tax Identification Numbers (ITINs).

Jeffrey A. Porter and American Institute of Certified Public Accountants. Tax Executive Committee

-

. by Jeffrey A. Porter and American Institute of Certified Public Accountants. Tax Executive Committee")

Letter From Jeffrey A. Porter, CPA, Chair, AICPA Tax Executive Committee, to Steven T. Miller, IRS Acting Commissioner; William J. Wilkins, IRS Chief Counsel; Curtis G. Wilson, IRS Associate Chief Counsel for Passthroughs and Special Industries; and Lisa Zarlenga, Tax Legislative Counsel, Department of the Treasury, Re: Comments on REG-130507-11 relating to guidance under section 1411, as added by the Health Care and Education Reconciliation Act of 2010, regarding net investment income tax as relevant to estates and trusts (12/5/2012).

Jeffrey A. Porter and American Institute of Certified Public Accountants. Tax Executive Committee

-

Letter from Jeffrey A. Porter, CPA, Chair, AICPA Tax Executive Committee, to Tom Udall, Chairman, and Mike Johanns, Ranking Member, Senate Appropriations Subcommittee on Financial Services and General Government; Ander Crenshaw, Chairman, and Jose Serrano, Ranking Member, House Appropriations Subcommittee on Financial Services and General Government, Re: IRS Fiscal Year 2014 Budget.

Jeffrey A. Porter and American Institute of Certified Public Accountants. Tax Executive Committee

-

, Internal Revenue Service, Re: Comments and Recommendations for Procedural Changes in Response to Ambiguities Raised in Complying with Final Regulations Under Sections 381(c)(4) and 381(c)(5)(TD 9534). by Jeffrey A. Porter and American Institute of Certified Public Accountants. Tax Executive Committee")

Letter from Jeffrey A. Porter, CPA, Chief, AICPA Tax Executive Committee, to Andrew Kelso, Jr., Associate Chief Counsel (Income Tax & Accounting), Internal Revenue Service, Re: Comments and Recommendations for Procedural Changes in Response to Ambiguities Raised in Complying with Final Regulations Under Sections 381(c)(4) and 381(c)(5)(TD 9534).

Jeffrey A. Porter and American Institute of Certified Public Accountants. Tax Executive Committee

-

")

Spring Meeting of Council, May 16 - 18, 2012, Volume 1, JW Marriott Hotel, 1331 Pennsylvania Avenue NW, Washington, D.C.

American Institute of Certified Public Accountants (AICPA)

-

")

Spring Meeting of Council, May 16 - 18, 2012, Volume 2, JW Marriott Hotel, 1331 Pennsylvania Avenue NW, Washington, D.C

American Institute of Certified Public Accountants (AICPA)

-

, Patricia A. Thompson, and American Institute of Certified Public Accountants. Tax Executive Committee")

Written Statement for the U.S. House of Representatives; Committee on Small Business; Subcommittee on Economic Growth, Tax and Capital Access; Public Hearing: Planning for the Death Tax: Can Small Businesses Survive; May 31, 2012.

American Institute of Certified Public Accountants (AICPA), Patricia A. Thompson, and American Institute of Certified Public Accountants. Tax Executive Committee

-

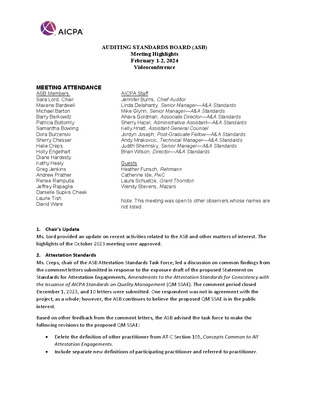

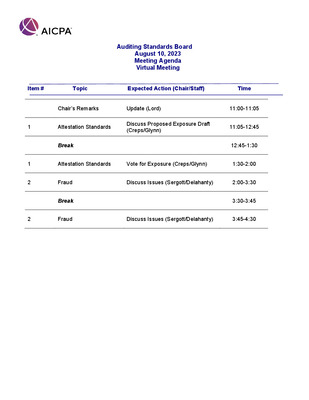

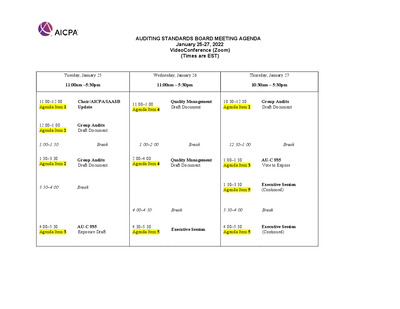

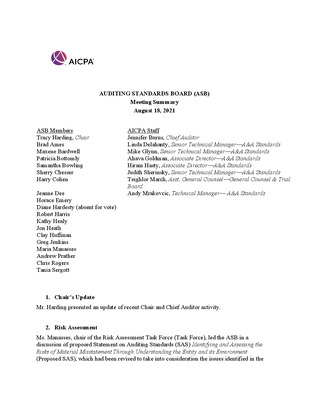

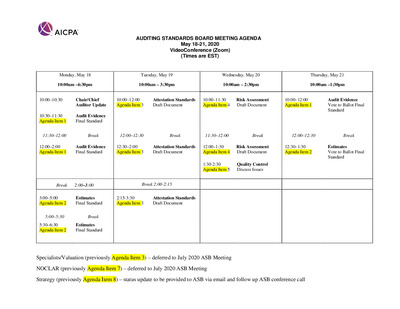

Accounting Standards Board, Conference Call, August 16, 2012 10am – 1pm Eastern, Meeting Agenda

American Institute of Certified Public Accountants. Auditing Standards Board

-

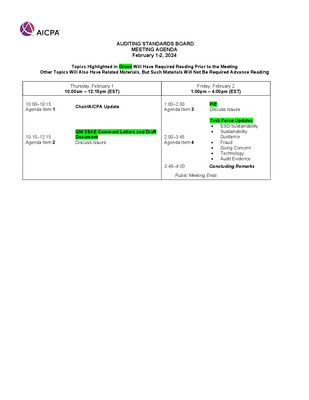

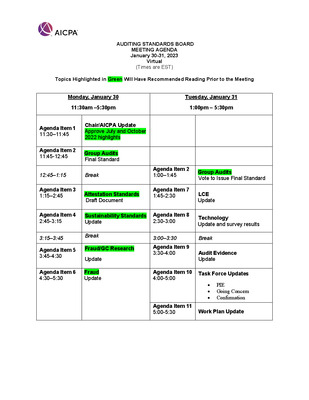

Agenda. Auditing Standards Board, January 10-12, 2012, Meeting San Juan, Puerto Rico

American Institute of Certified Public Accountants. Auditing Standards Board

-

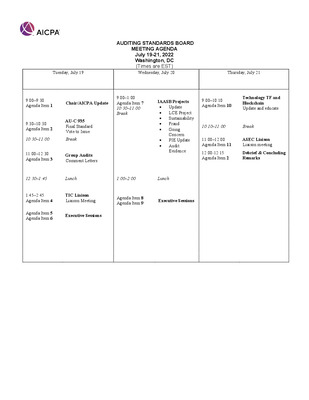

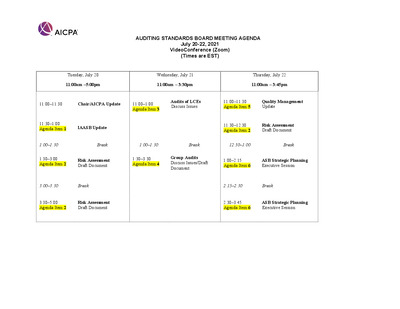

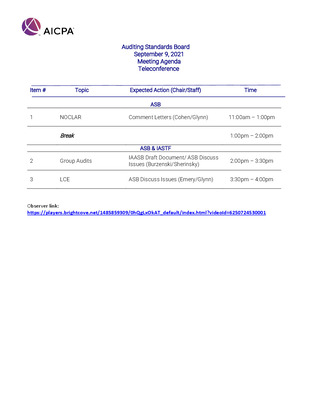

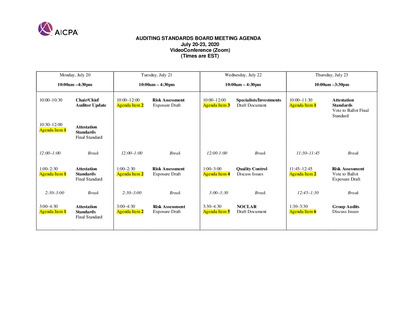

Agenda, Auditing Standards Board, July 31-August 2, 2012 Meeting, Minneapolis, MN

American Institute of Certified Public Accountants. Auditing Standards Board

-

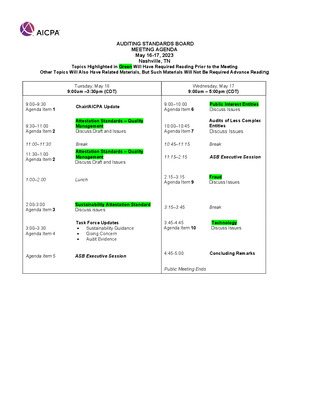

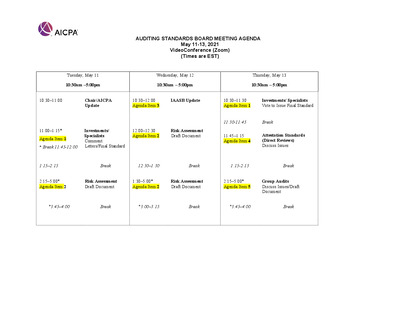

Agenda, Auditing Standards Board, May 1-3, 2012, Meeting Boston, MA

American Institute of Certified Public Accountants. Auditing Standards Board

-

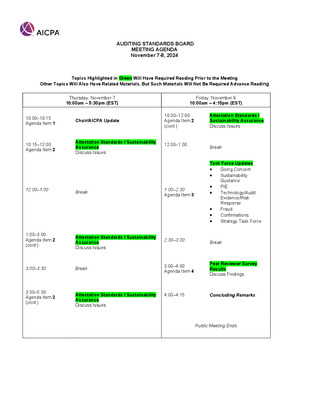

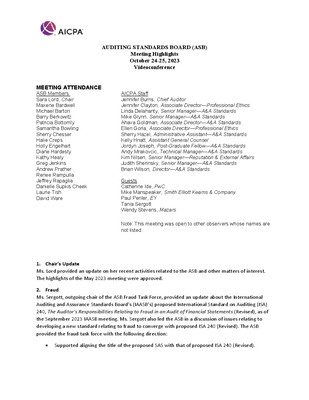

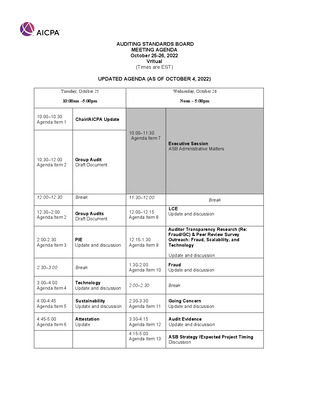

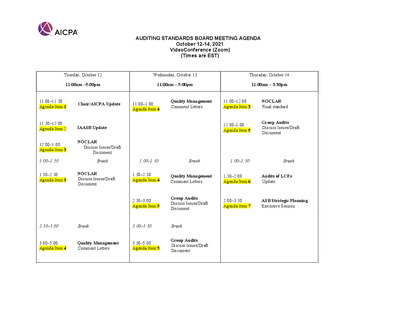

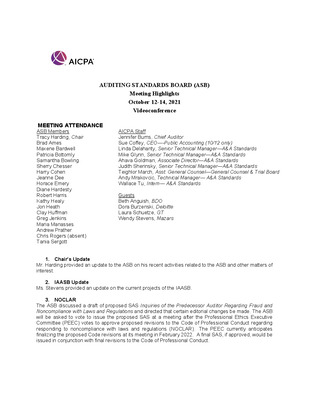

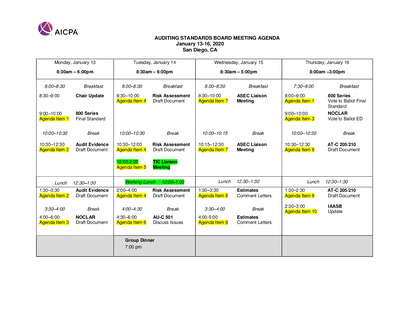

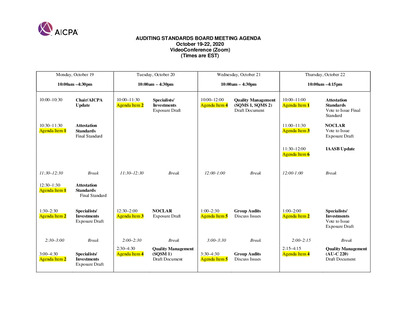

Agenda, Auditing Standards Board, October 16-18, 2012 Meeting, Cleveland, OH

American Institute of Certified Public Accountants. Auditing Standards Board

-

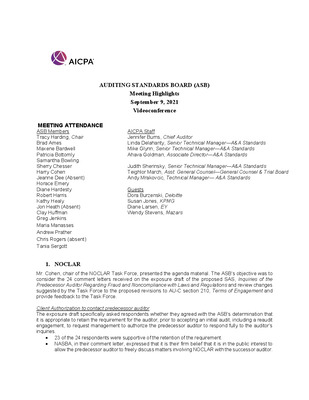

meeting, August 16, 2012 Teleconference; Highlights (ASB) meeting, August 16, 2012 by American Institute of Certified Public Accountants. Auditing Standards Board")

Auditing Standards Board (ASB) meeting, August 16, 2012 Teleconference; Highlights (ASB) meeting, August 16, 2012

American Institute of Certified Public Accountants. Auditing Standards Board

-

meeting, January 10-12, 2012, San Juan, Puerto Rico (Final); Highlights (ASB) meeting, January 10-12, 2012 (Final) by American Institute of Certified Public Accountants. Auditing Standards Board")

Auditing Standards Board (ASB) meeting, January 10-12, 2012, San Juan, Puerto Rico (Final); Highlights (ASB) meeting, January 10-12, 2012 (Final)

American Institute of Certified Public Accountants. Auditing Standards Board

-

meeting, July 31- August 2, 2012, Minneapolis, MN; Highlights (ASB) meeting, July 31- August 2, 2012 by American Institute of Certified Public Accountants. Auditing Standards Board")

Auditing Standards Board (ASB) meeting, July 31- August 2, 2012, Minneapolis, MN; Highlights (ASB) meeting, July 31- August 2, 2012

American Institute of Certified Public Accountants. Auditing Standards Board

-

meeting, May 1-3, 2012, Boston, MA, San Juan, Puerto Rico; Highlights (ASB) meeting, May 1-3, 2012 by American Institute of Certified Public Accountants. Auditing Standards Board")

Auditing Standards Board (ASB) meeting, May 1-3, 2012, Boston, MA, San Juan, Puerto Rico; Highlights (ASB) meeting, May 1-3, 2012

American Institute of Certified Public Accountants. Auditing Standards Board

-

meeting, November 28, 2012 Conference Call; Highlights (ASB) meeting, November 28, 2012 by American Institute of Certified Public Accountants. Auditing Standards Board")

Auditing Standards Board (ASB) meeting, November 28, 2012 Conference Call; Highlights (ASB) meeting, November 28, 2012

American Institute of Certified Public Accountants. Auditing Standards Board

-

meeting, October 16-18, 2012, Cleveland, OH; Highlights (ASB) meeting, October 16-18, 2012 by American Institute of Certified Public Accountants. Auditing Standards Board")

Auditing Standards Board (ASB) meeting, October 16-18, 2012, Cleveland, OH; Highlights (ASB) meeting, October 16-18, 2012

American Institute of Certified Public Accountants. Auditing Standards Board

-

AICPA Comment Letter, Re: PCAOB Rulemaking Docket Matter No. 039.

American Institute of Certified Public Accountants. Public Practice and Global Alliances

-

, 168, and 263(a) Regarding Deduction and Capitalization of Expenditures Related to Tangible Property (REG-168745-03 and TD 9564) and Revenue Procedures 2012-19 and 2012-20 by American Institute of Certified Public Accountants. Repair Regulations Task Force")

RE: Comments on Proposed and Temporary Regulations under Sections 162(a), 168, and 263(a) Regarding Deduction and Capitalization of Expenditures Related to Tangible Property (REG-168745-03 and TD 9564) and Revenue Procedures 2012-19 and 2012-20

American Institute of Certified Public Accountants. Repair Regulations Task Force

-

. by Thomas Burrage and American Institute of Certified Public Accountants. Forensic and Valuation Services Executive Committee")

Letter from Thomas Burrage, CPA, Chair, AICPA Forensic and Valuation Services Executive Committee, to Appraisal Standards Board, The Appraisal Foundation, Re: Exposure Draft of the Proposed Changes to the 2014-15 Edition of the Uniform Standards of Professional Appraisal Practice (USPAP).

Thomas Burrage and American Institute of Certified Public Accountants. Forensic and Valuation Services Executive Committee

-

Comment on Internal Control Over External Financial Reporting and Internal Control-Integrated Framework

Committee of Sponsoring Organizations of the Treadway Commission

-

Internal Control—Integrated Framework: Feedback Questions, September 2012

Committee of Sponsoring Organizations of the Treadway Commission

-

Internal Control—Integrated Framework: Framework and Appendices, September 2012

Committee of Sponsoring Organizations of the Treadway Commission

-

Internal Control—Integrated Framework: Illustrative Tools for Assessing Effectiveness of a System of Internal Control, September 2012

Committee of Sponsoring Organizations of the Treadway Commission

-

Internal Control — Integrated Framework: Internal Control over External Financial Reporting: A Compendium of Approaches and Examples, September 2012

Committee of Sponsoring Organizations of the Treadway Commission

-

Risk Assessment in Practice

Deloitte & Touche, Patchin Curtis, Mark Carey, and Committee of Sponsoring Organizations of the Treadway Commission

-

Letter from Jeffrey A. Porter, CPA, Chair, AICPA Tax Executive Committee, to Douglas H. Shulman, IRS Commissioner, Re: Request for Further Relief Due to Hurricane Sandy for Various Tax and Information Returns and Payments Otherwise Due November 15, 2012 and Beyond.

Jeffrey A. Porter and American Institute of Certified Public Accountants. Tax Executive Committee

-

Enterprise Risk Management: Understanding and Communicating Risk Appetite

Larry Rittenberg, Frank Martens, and Committee of Sponsoring Organizations of the Treadway Commission

-

and Rev. Proc. 97-27 Section 3.08(4). by Patricia A. Thompson and American Institute of Certified Public Accountants. Tax Executive Committee")

Letter From Patricia A. Thompson, Chair, AICPA Tax Executive Committee, to Lisa Zarlenga, Tax Legislative Counsel, Department of the Treasury, Re: Comments on the Definition of Issue Under Consideration--Certain Foreign Corporations Contained in Rev. Proc. 2011-14, Section 3.09(4) and Rev. Proc. 97-27 Section 3.08(4).

Patricia A. Thompson and American Institute of Certified Public Accountants. Tax Executive Committee

-

Letter From Patricia A. Thompson, CPA, Chair, AICPA Tax Executive Committee, to Dave Camp, Chairman, House Committee on Ways & Means, and Sander M. Levin, Ranking Member, House Committee on Ways & Means, Re: Support for H.R. 5630, Fighting Tax Fraud Act of 2012.

Patricia A. Thompson and American Institute of Certified Public Accountants. Tax Executive Committee

-

Letter From Patricia A. Thompson, CPA, Chair, AICPA Tax Executive Committee, to Douglas H. Shulman, Commissioner, Internal Revenue Service, Re: Need for IRS Resolution to Systemic IRS Incorrect Letters on Form 3520.

Patricia A. Thompson and American Institute of Certified Public Accountants. Tax Executive Committee

-

Application Process. by Patricia A. Thompson and American Institute of Certified Public Accountants. Tax Executive Committee")

Letter From Patricia A. Thompson, CPA, Chair, AICPA Tax Executive Committee, to Douglas H. Shulman, Commissioner, IRS, Re: IRS Announcement on June 22, 2012, Regarding Interim Changes to the Individual Taxpayer Identification Number (ITIN) Application Process.

Patricia A. Thompson and American Institute of Certified Public Accountants. Tax Executive Committee

-

Letter From Patricia Thompson, CPA, Chair, AICPA Tax Executive Committee, to Ruth Perez, Deputy Commissioner, Small Business/Self-Employed Division, Internal Revenue Service, Re: Conference Call Regarding Forms 1099-B and the Reporting of a Customer's Basis When a Security is Sold.

Patricia A. Thompson and American Institute of Certified Public Accountants. Tax Executive Committee

-

, 168, and 263(a) Regarding Deduction and Capitalization of Expenditures Related to Tangible Property (REG-168745-03 and TD 9564) and Revenue Procedures 2012-19 and 2012-20. by Patricia A. Thompson and American Institute of Certified Public Accountants. Tax Executive Committee.")

Letter from Patricia A. Thompson, CPA, Chair, AICPA Tax Executive Committee, to Internal Revenue Service, Re: Comments on Proposed and Temporary Regulations Under Section 162(a), 168, and 263(a) Regarding Deduction and Capitalization of Expenditures Related to Tangible Property (REG-168745-03 and TD 9564) and Revenue Procedures 2012-19 and 2012-20.

Patricia A. Thompson and American Institute of Certified Public Accountants. Tax Executive Committee.

-

. by Patricia A. Thompson and American Institute of Certified Public Accountants.Tax Executive Committee")

Letter from Patricia A. Thompson, CPA, Chair, AICPA Tax Executive Committee, Re: Comments on REG-112196-07 Regarding Guidance on the Estate Tax Election to Use the Alternate Valuation Method Under Section 2032, Notice of Proposed Rulemaking (11/17/2011).

Patricia A. Thompson and American Institute of Certified Public Accountants.Tax Executive Committee

-

, Internal Revenue Service, Re: Recommendation for Modification of Rev. Proc. 2011-18 Concerning the Accounting Method for Income from Gift Card Receipts. by Patricia A. Thompson and American Institute of Certified Public Accountants. Tax Executive Committee cc:")

Letter from Patricia A. Thompson, CPA, Chair, AICPA Tax Executive Committee, to Andrew Keyso, Jr., Associate Chief Counsel (Income Tax & Accounting), Internal Revenue Service, Re: Recommendation for Modification of Rev. Proc. 2011-18 Concerning the Accounting Method for Income from Gift Card Receipts.

Patricia A. Thompson and American Institute of Certified Public Accountants. Tax Executive Committee cc:

-

and National Association of State Boards of Accountancy")

Uniform Accountancy Act, Standards for Regulation Including Substantial Equivalency

American Institute of Certified Public Accountants (AICPA) and National Association of State Boards of Accountancy

-

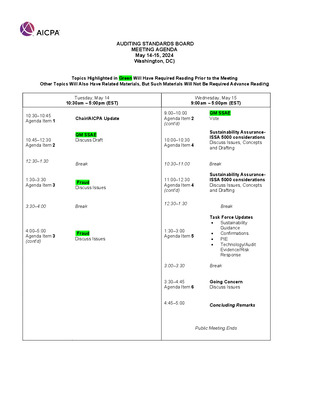

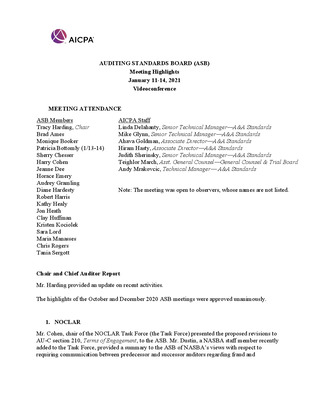

Agenda, Auditing Standards Board, January 11-13, 2011, Meeting San Juan, Puerto Rico

American Institute of Certified Public Accountants. Auditing Standards Board

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}