{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

-

Comment Letters on Proposed Statements on Auditing Standards—Auditor Reporting: Forming an Opinion and Reporting on Financial Statements, Communicating Key Audit Matters in the Independent Auditor’s Report, Modifications to the Opinion in the Independent Auditor’s Report, Emphasis-of-Matter Paragraphs and Other-Matter Paragraphs in the Independent Auditor’s Report, Proposed Amendments—Addressing Disclosures in the Audit of Financial Statements, November 28, 2017

American Institute of Certified Public Accountants. Auditing Standards Board

-

Comment Letters on Proposed new and revised definitions and interpretations Compliance audits New definition "compliance audit" New definition "compliance audit attest client" Revised definition "financial statement attest client" Revised "Client Affiliates" interpretation Revised "State and Local Governments Client Affiliates" interpretation June 3, 2022

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

Revised \"Conceptual Framework for Members in Public Practice\" (1.000.010), June 3, 2022 by American Institute of Certified Public Accountants. Professional Ethics Executive Committee")

Comment Letters on Proposed revisions related to officers, directors, and beneficial owners Revised "Offering or Accepting Gifts or Entertainment interpretations (1.120.010 and 1.285.010) Revised "Conceptual Framework for Members in Public Practice" (1.000.010), June 3, 2022

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

Exposure draft: Proposed new and revised definitions and interpretations Compliance audits New definition "compliance audit" New definition "compliance audit attest client" Revised definition "financial statement attest client" Revised "Client Affiliates" interpretation Revised "State and Local Governments Client Affiliates" interpretation June 3, 2022, Comments are requested by September 1, 2022

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

Revised \"Conceptual Framework for Members in Public Practice\" (1.000.010), June 3, 2022, Comments are requested by July 5, 2022 by American Institute of Certified Public Accountants. Professional Ethics Executive Committee")

Exposure draft: Proposed revisions related to officers, directors, and beneficial owners Revised "Offering or Accepting Gifts or Entertainment interpretations (1.120.010 and 1.285.010) Revised "Conceptual Framework for Members in Public Practice" (1.000.010), June 3, 2022, Comments are requested by July 5, 2022

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

, September 2022 by American Institute of Certified Public Accountants. Professional Ethics Executive Committee")

Technical correction Section 529 Plans (ET sec. 1.240.070), September 2022

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

, 2021, September 15 by American Institute of Certified Public Accountants. Professional Ethics Executive Committee")

Accounting Standards Implementation Services September 20, 2021 Comments are requested by December 20, 2021, Exposure draft (American Institute of Certified Public Accountants), 2021, September 15

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

Comment Letters on Accounting Standards Implementation Services September 20, 2021

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

Comment Letters on Proposed interpretations and definition: Responding to Noncompliance With Laws and Regulations, February 25, 2021

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

Comment Letters on Proposed revised interpretations and definition: Loans, acquisitions, and other transactions Definition of "beneficially owned" "Client Affiliates" interpretation "Loans"” interpretation "Loans and Leases With Lending Institutions" interpretation "Immediate Family Members" interpretation, October 5, 2021,

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

Comment Letters on Proposed revised interpretation, Unpaid Fees September 20, 2021

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

Official Release: Temporary Policy Statement Related to Amendments of Rule 2-01 of Regulation S-X, Adopted December 21, 2020

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

, 2021, February 25 by American Institute of Certified Public Accountants. Professional Ethics Executive Committee")

Proposed interpretations and definition: Responding to Noncompliance With Laws and Regulations, February 25, 2021, Comments are requested by June 30, 2021; Exposure draft (American Institute of Certified Public Accountants), 2021, February 25

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

, 2021, October 5 by American Institute of Certified Public Accountants. Professional Ethics Executive Committee")

Proposed revised interpretations and definition: Loans, acquisitions, and other transactions Definition of "beneficially owned" "Client Affiliates" interpretation "Loans"” interpretation "Loans and Leases With Lending Institutions" interpretation "Immediate Family Members" interpretation, October 5, 2021, Comments are requested by January 5, 2022; Exposure draft (American Institute of Certified Public Accountants), 2021, October 5

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

, 2021, September15 by American Institute of Certified Public Accountants. Professional Ethics Executive Committee")

Proposed revised interpretation, Unpaid Fees September 20, 2021, Comments are requested by December 20, 2021, Exposure draft (American Institute of Certified Public Accountants), 2021, September15

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

Comment Letters on Proposed Statement on Auditing Standards, Amendments to AU-C Sections 501, 540, and 620 Related to the Use of Specialists and the Use of Pricing Information Obtained from External Information Sources, November 4, 2020

American Institute of Certified Public Accountants. Auditing Standards Board

-

Ballots for Proposed Statement on Auditing Standards, Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement, August 27, 2020

American Institute of Certified Public Accountants. Auditing Standards Board

-

Comment Letters on Proposed Statement on Auditing Standards, Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement, August 27, 2020

American Institute of Certified Public Accountants. Auditing Standards Board

-

. 2020, November 4 by American Institute of Certified Public Accountants. Auditing Standards Board")

Proposed Statement on Auditing Standards, Amendments to AU-C Sections 501, 540, and 620 Related to the Use of Specialists and the Use of Pricing Information Obtained from External Information Sources, November 4, 2020, Comments are requested by February 4, 2021; Exposure Draft (American Institute of Certified Public Accountants). 2020, November 4

American Institute of Certified Public Accountants. Auditing Standards Board

-

, 2020, August 27 by American Institute of Certified Public Accountants. Auditing Standards Board")

Proposed Statement on Auditing Standards, Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement, August 27, 2020, Comments are requested by November 25, 2020; Exposure draft (American Institute of Certified Public Accountants), 2020, August 27

American Institute of Certified Public Accountants. Auditing Standards Board

-

Materiality considerations for attestation engagements involving aspects of subject matters that cannot be quantitatively measured

American Institute of Certified Public Accountants. Materiality Working Group

-

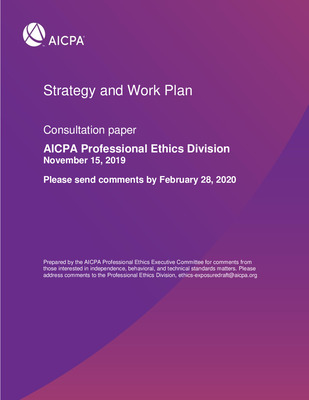

AICPA Professional Ethics Division: Strategy and Work Plan for 2021-2023, November 25, 2020

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

Comment Letters on Proposed interpretation: Staff Augmentation Arrangements, September 8, 2020

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

Comment Letters on Proposed revised interpretation: Records Requests, May 1, 2020

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

, 2020, September 8 by American Institute of Certified Public Accountants. Professional Ethics Executive Committee")

Proposed interpretation: Staff Augmentation Arrangements, September 8, 2020. Comments are requested by December 8, 2020; Exposure draft (American Institute of Certified Public Accountants), 2020, September 8

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

, 2020, May 1 by American Institute of Certified Public Accountants. Professional Ethics Executive Committee")

Proposed revised interpretation: Records Requests, May 1, 2020, Comments are requested by September 30, 2020; Exposure draft (American Institute of Certified Public Accountants), 2020, May 1

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

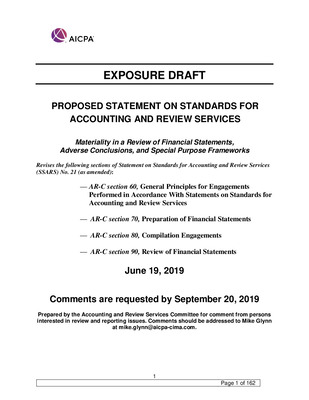

Comment Letters on Proposed Statement on Standards for Accounting and Review Services, Materiality in a review of financial Statements, Adverse conclusions, and special Purpose frameworks, June 19, 2019

American Institute of Certified Public Accountants. Accounting and Review Services Committee

-

, 2019, June 19 by American Institute of Certified Public Accountants. Accounting and Review Services Committee")

Proposed Statement on Standards for Accounting and Review Services, Materiality in a review of financial Statements, Adverse conclusions, and special Purpose frameworks, June 19, 2019, Comments are requested by September 20, 2019; Exposure draft (American Institute of Certified Public Accountants), 2019, June 19

American Institute of Certified Public Accountants. Accounting and Review Services Committee

-

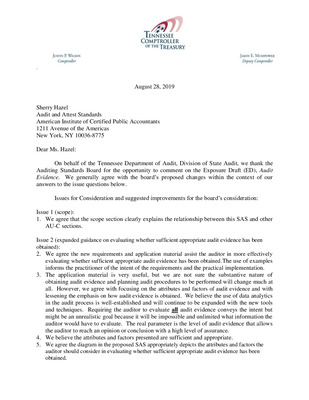

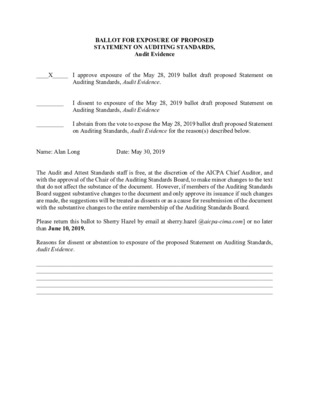

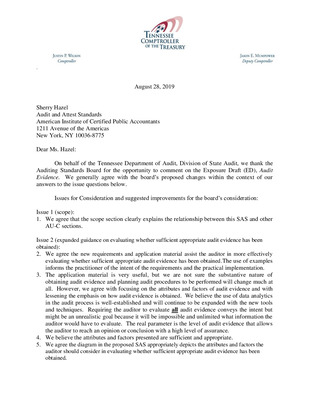

Comment Letters on Proposed Statement on Auditing Standards: Auditing Evidence, June 20, 2019, Comments are requested by September 18, 2019

American Institute of Certified Public Accountants. Auditing Standards Board

-

Ballots for Proposed Statement on Auditing Standards, Audit Evidence, June 20, 2019, Comments are requested by September 18, 2019

American Institute of Certified Public Accountants. Auditing Standards Board

-

Ballots for Proposed Statement on Auditing Standards, Auditing Accounting Estimates and Other Disclosures, August 22, 2019

American Institute of Certified Public Accountants. Auditing Standards Board

-

Comment Letters on Discussion Paper - Materiality Considerations for Attestation Engagements Involving Aspects of Subject Matters That Cannot Be Quantitatively Measured

American Institute of Certified Public Accountants. Auditing Standards Board

-

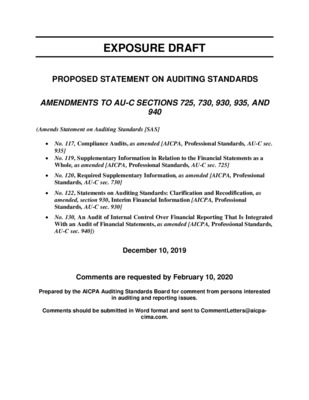

Comment Letters on Proposed Statement on Auditing Standards, Amendments to AU-C Sections 725, 730, 930, 935, and 940, December 10, 2019

American Institute of Certified Public Accountants. Auditing Standards Board

-

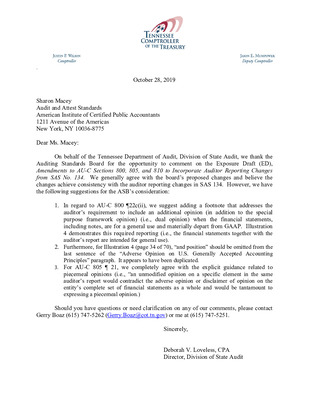

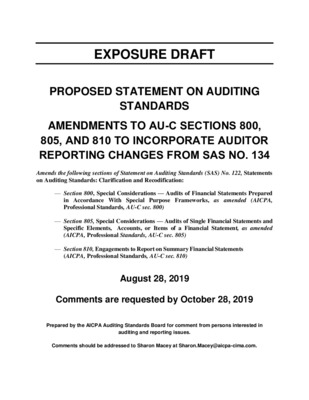

Comment Letters on Proposed Statement on Auditing Standards, Amendments to AU-C Sections 800, 805, and 810 to Incorporate Auditor Reporting Changes from SAS No. 134, August 28, 2019

American Institute of Certified Public Accountants. Auditing Standards Board

-

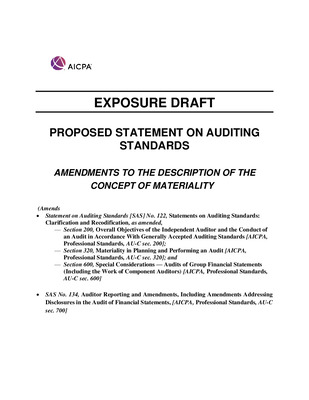

Comment Letters on Proposed Statement on Auditing Standards, Amendments to the Description of the Concept of Materiality, June 5, 2019

American Institute of Certified Public Accountants. Auditing Standards Board

-

Comment Letters on Proposed Statement on Auditing Standards, Audit Evidence, June 20, 2019, Comments are requested by September 18, 2019

American Institute of Certified Public Accountants. Auditing Standards Board

-

Comment Letters on Proposed Statement on Auditing Standards, Auditing Accounting Estimates and Other Disclosures, August 22, 2019

American Institute of Certified Public Accountants. Auditing Standards Board

-

Comment Letters on Proposed strategy and work plan

American Institute of Certified Public Accountants. Auditing Standards Board

-

, 2019, December 10 by American Institute of Certified Public Accountants. Auditing Standards Board")

Proposed Statement on Auditing Standards, Amendments to AU-C Sections 725, 730, 930, 935, and 940, December 10, 2019, Comments are requested by February 10, 2020; Exposure draft (American Institute of Certified Public Accountants), 2019, December 10

American Institute of Certified Public Accountants. Auditing Standards Board

-

, 2019, August 28 by American Institute of Certified Public Accountants. Auditing Standards Board")

Proposed Statement on Auditing Standards, Amendments to AU-C Sections 800, 805, and 810 to Incorporate Auditor Reporting Changes from SAS No. 134, August 28, 2019, Comments are requested by October 28, 2019; Exposure draft (American Institute of Certified Public Accountants), 2019, August 28

American Institute of Certified Public Accountants. Auditing Standards Board

-

, 2019, June 5 by American Institute of Certified Public Accountants. Auditing Standards Board")

Proposed Statement on Auditing Standards, Amendments to the Description of the Concept of Materiality, June 5, 2019, Comments are requested by August 5, 2019; Exposure draft (American Institute of Certified Public Accountants), 2019, June 5

American Institute of Certified Public Accountants. Auditing Standards Board

-

, 2019, June 20 by American Institute of Certified Public Accountants. Auditing Standards Board")

Proposed Statement on Auditing Standards, Audit Evidence, June 20, 2019, Comments are requested by September 18, 2019; Exposure draft (American Institute of Certified Public Accountants), 2019, June 20

American Institute of Certified Public Accountants. Auditing Standards Board

-

, 2019, August 22 by American Institute of Certified Public Accountants. Auditing Standards Board")

Proposed Statement on Auditing Standards, Auditing Accounting Estimates and Other Disclosures, August 22, 2019. Comments are requested by November 22, 2019; Exposure draft (American Institute of Certified Public Accountants), 2019, August 22

American Institute of Certified Public Accountants. Auditing Standards Board

-

, 2019, June 20 by American Institute of Certified Public Accountants. Auditing Standards Board")

Proposed Statement on Auditing Standards: Auditing Evidence, June 20, 2019, Comments are requested by September 18, 2019; Exposure Draft (American Institute of Certified Public Accountants), 2019, June 20

American Institute of Certified Public Accountants. Auditing Standards Board

-

Proposed strategy and work plan

American Institute of Certified Public Accountants. Auditing Standards Board

-

, January 11, 2019 by American Institute of Certified Public Accountants. Professional Ethics Executive Committee")

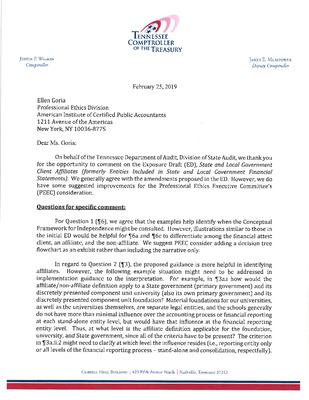

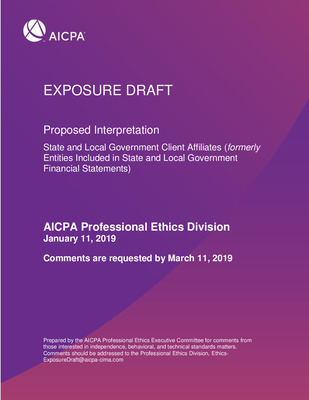

Comment Letters on Proposed Interpretation: State and Local Government Client Affiliates (formerly Entities Included in State and Local Government Financial Statements), January 11, 2019

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

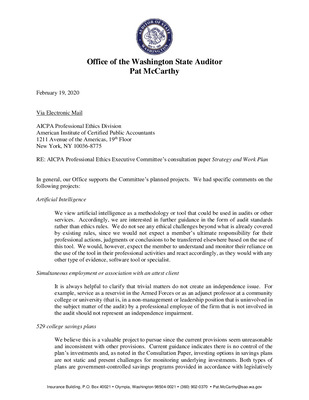

Comment Letters on Strategy and Work Plan: Consultation paper, AICPA Professional Ethics Division, November 15, 2019

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

-

, January 11, 2019 ,Comments are requested by March 11, 2019; Exposure draft (American Institute of Certified Public Accountants),, 2019, January 11 by American Institute of Certified Public Accountants. Professional Ethics Executive Committee")

Proposed Interpretation: State and Local Government Client Affiliates (formerly Entities Included in State and Local Government Financial Statements), January 11, 2019 ,Comments are requested by March 11, 2019; Exposure draft (American Institute of Certified Public Accountants),, 2019, January 11

American Institute of Certified Public Accountants. Professional Ethics Executive Committee