-

, 1998, Oct. 16 by American Institute of Certified Public Accountants. Accounting Standards Executive Committee")

Proposed statement of position : accounting by producers and distributors of films;Accounting by producers and distributors of films; Exposure draft (American Institute of Certified Public Accountants), 1998, Oct. 16

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

This proposed Statement of Position (SOP) provides guidance on accounting by producers and distributors of motion picture films. This proposed SOP requires the following: 1. Revenue should be recognized when all of the following conditions are met: a. Persuasive evidence of a sale or licensing arrangement with a customer exists. b. The film is complete and, in accordance with the terms of the arrangement, either has been delivered or is available to be delivered. c. The license period of the arrangement has begun and the customer can begin its exploitation or exhibition. d. The gross revenue is fixed or determinable. e. Collection is reasonably assured. Licensing arrangements that meet all of the above conditions and transfer substantially all of the benefits and risks incident to ownership of the film on an exclusive basis for an individual market and territory should be accounted for as sales. In arrangements that do not meet the "substantially all" and exclusivity requirements, but meet all of the conditions above, revenue should be recognized ratably over the licensing period unless another systematic and rational basis is more representative of the time pattern in which use benefit from the licensed film is diminished, in which case that basis should be used. 2. The costs of producing a film and bringing that film to market consist of production costs, exploitation costs, and participation costs. The present value of participation costs should be accrued when their payment is probable, which is usually determined when the film has been released. Entities should recognize an asset as part of film costs for the initial amount of the participation liability. Production costs and capitalized participation costs should be amortized using the individual-film-forecast-computation method. The individual-film-forecast-computation method requires estimating remaining ultimate gross revenues (original estimates should not exceed 10 years, and amounts included are subject to limitations) as of the beginning of each period. It also requires determining a fraction, the numerator of which is actual gross revenues from the film for the current period and the denominator of which is the estimated unrecognized ultimate gross revenues as of the beginning of the period. This fraction is applied to the unamortized balance of production costs and capitalized participation costs as of the beginning of the period to determine periodic amortization. In this way, in the absence of changes in estimates, production costs and capitalized participation costs are amortized in a manner that yields a constant rate of profit for each film, excluding exploitation costs and other period expenses. Amortization should begin when a film is released and revenues from that film are recognized. Prerelease and early release exploitation costs incurred on a territory-by-territory basis in the theatrical market should be capitalized and amortized over the expected period of exploitation of the film in that theatrical market and territory, not to exceed three months from release date. Capitalized exploitation costs for a particular territory should be amortized in the same ratio that theatrical gross revenues earned in that particular theatrical territory bear to estimated total theatrical gross revenues for that territory for the shorter of (a) three months or {b) the theatrical release period in that territory. All capitalized exploitation costs should be fully amortized by the end of the theatrical release period or three months (whichever is shorter). Exploitation costs should not be accrued in advance of incurrence. After the period leading up to the theatrical release of a film in a territory and the initial three-month period, all exploitation costs should be expensed as incurred. Exploitation costs incurred in connection with the release of a film in markets other than the theatrical market should be expensed as incurred. 3. Unamortized film costs should be reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of the film may not be recoverable, in accordance with Financial Accounting Standards Board (FASB) Statement No. 121, Accounting for the Impairment of Long-Lived Assets and for Long-Lived Assets to Be Disposed Of. 4. Certain disclosures should be made in the financial statements or notes thereto. This SOP is effective for financial statements for fiscal years beginning after December 1 5, 1 999, with earlier application encouraged. The cumulative effect of changes in accounting principle caused by adopting the provisions of this SOP should be included in the determination of net income in conformity with paragraph 20 of Accounting Principles Board Opinion No. 20, Accounting Changes.

-

, 1998,August 20 by American Institute of Certified Public Accountants. Accounting Standards Executive Committee")

Proposed statement of position : accounting by producers and distributors of films; Exposure draft (American Institute of Certified Public Accountants), 1998,August 20

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

Reporting on the Costs of Start-up Activities, Draft Dated 1/8/1998, Sent to FASB

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

Reporting on the costs of start-up activities; Statement of position 98-5;

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

, 1998, Feb. 11 by American Institute of Certified Public Accountants. Accounting Standards Executive Committee and American Institute of Certified Public Accountants. Software Revenue Recognition Working Group")

Proposed statement of position : Deferral of the effective date of certain provisions of SOP 97-2, Software revenue recognition, for certain transactions ;Deferral of the effective date of certain provisions of SOP 97-2, Software revenue recognition, for certain transactions; Exposure draft (American Institute of Certified Public Accountants), 1998, Feb. 11

American Institute of Certified Public Accountants. Accounting Standards Executive Committee and American Institute of Certified Public Accountants. Software Revenue Recognition Working Group

This proposed Statement of Position (SOP) defers for one year the application of paragraph 10 of SOP 97-2, Software Revenue Recognition, with respect to what constitutes vendor-specific objective evidence of the fair value of the delivered software element in certain multiple-element arrangements that include service elements and that are entered into by entities that never sell the software element separately. All other provisions of SOP 97-2 remain in effect even for the kinds of transactions described in this SOP.

-

;Modification of the limitations on evidence of fair value in software arrangements : (a proposed amendment to SOP 97-2, Software revenue recognition); Exposure draft (American Institute of Certified Public Accountants), 1998, July 31 by American Institute of Certified Public Accountants. Accounting Standards Executive Committee and American Institute of Certified Public Accountants. Software Revenue Recognition Working Group")

Proposed Statement of Position : Modification of the limitations on evidence of fair value in software arrangements : (a proposed amendment to SOP 97-2, Software revenue recognition) ;Modification of the limitations on evidence of fair value in software arrangements : (a proposed amendment to SOP 97-2, Software revenue recognition); Exposure draft (American Institute of Certified Public Accountants), 1998, July 31

American Institute of Certified Public Accountants. Accounting Standards Executive Committee and American Institute of Certified Public Accountants. Software Revenue Recognition Working Group

This Statement of Position (SOP) rescinds the second sentences of paragraphs 10, 37, 41, and 57 of SOP 97-2, Software Revenue Recognition, which limited what is considered vendor-specific objective evidence of the fair value of the various elements in a multiple-element arrangement. This SOP also amends certain examples in SOP 97-2 for the rescission of these sentences, and it adds one example. All other provisions of SOP 97-2 remain in effect. This SOP is effective for transactions entered into in fiscal years beginning after December 1 5, 1998.

-

")

Comment letters on Modification of the Limitations on Evidence of Fair Value in Software Arrangements

American Institute of Certified Public Accountants (AICPA)

-

")

Comment letters on Proposed Audit and Accounting Guide “Audits of Investment Companies"

American Institute of Certified Public Accountants (AICPA)

-

")

Comment letters on Restricting the Use of an Auditor's Report

American Institute of Certified Public Accountants (AICPA)

-

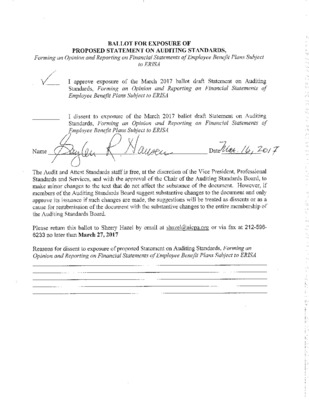

, Amendments to SSAE Nos. 1, 2 and 3. by American Institute of Certified Public Accountants. Auditing Standards Board")

Comment letters on Proposed Statement on Standards for Attestation Engagements (SSAE), Amendments to SSAE Nos. 1, 2 and 3.

American Institute of Certified Public Accountants. Auditing Standards Board

-

, 1998, Jan. 26 by American Institute of Certified Public Accountants. Auditing Standards Board")

Proposed statement on auditing standards : restricting the use of an auditor's report : and amendments of SAS No. 60, communication of internal control related matters noted in an audit, and SAS No. 75, engagements to apply agreed-upon procedures to specified elements, accounts, or items of a financial statement ;Restricting the use of an auditor's report : and amendments of SAS No. 60, communication of internal control related matters noted in an audit, and SAS No. 75, engagements to apply agreed-upon procedures to specified elements, accounts, or items of a financial statement; Exposure draft (American Institute of Certified Public Accountants), 1998, Jan. 26

American Institute of Certified Public Accountants. Auditing Standards Board

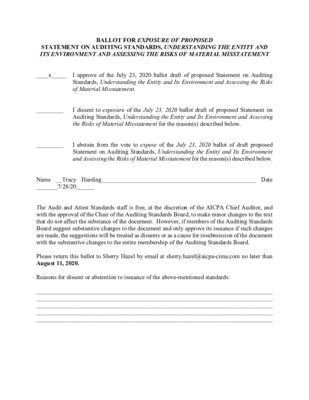

This proposed Statement provides guidance to auditors to enable them to determine whether an engagement requires a restricted-use report and, if so, what elements to include in that report. Existing auditing standards for engagements requiring restricted-use reports each contain guidance related to the applicable report. This Statement unifies that guidance. This proposed Statement: 1. Describes the circumstances in which the use of an auditor's report should be restricted. 2. Specifies the language to be used in a restricted-use report. 3. Presents the rationale for restricting the use of an auditor's report in each of the circumstances described. 4. Replaces the terms restricted distribution and general distribution with the terms restricted use and general use because auditors are not responsible for controlling the distribution of the reports they issue. 5. Defines the terms restricted use and general use. 6. Clarifies that an auditor may restrict the use of a report that ordinarily is a general-use report. 7. Requires that an auditor restrict a "combined" report if it covers subject matter or presentations that ordinarily do not require a restriction on use and subject matter or presentations that require such a restriction. It permits auditors to include a separate general-use report in a document that also contains a restricted-use report. 8. Amends paragraph 47 of SAS No. 75, Engagements to Apply Agreed-Upon Procedures to Specified Elements, Accounts, or Items of a Financial Statement (AICPA, Professional Standards, vol. 1, AU sec. 622), to permit the inclusion of a separate general-use report in a document containing an agreed-upon procedures report. This amendment does not change the requirement that an auditor restrict a "combined" report if it covers subject matter or presentations that ordinarily do not require a restriction on use and also covers agreed-upon procedures. See appendix A herein for the proposed amandment. 9. Deletes the words or other specified third party from the last sentence of the illustrative report in paragraph 12 of SAS No. 60, Communication of Internal Control Related Matters Noted in an Audit (AICPA, Professional Standards, vol. 1, AU sec. 325), because those words are inconsistent with the guidance in paragraph 10 of SAS No. 60, which does not provide for the addition of other specified third parties as report users. See appendix B herein for the proposed amendment. The proposed Statement would require that conforming changes be made to the guidance in the following documents: 1. SAS No. 51, Reporting on Financial Statements Prepared for Use in Other Countries (AICPA Professional Standards, vol. 1, AU sec. 534); 2. SAS No. 60, Communication of Internal Control Related Matters Noted in an Audit; 3. SAS No. 61, Communication With Audit Committees (AICPA, Professional Standards, vol. 1, AU sec. 380); 4. SAS No. 62, Special Reports (AICPA, Professional Standards, vol. 1, AU sec. 623); 5. SAS No. 75 Engagements to Apply Agreed-Upon Procedures to Specified Elements, Accounts, or Items of a Financial Statement.

-

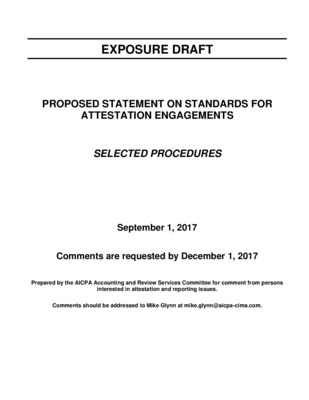

, 1998, June 1 by American Institute of Certified Public Accountants. Auditing Standards Board")

Proposed statement on standards for attestation engagements : amendments to Statement on standards for attestation engagements no. 1, Attestation standards, Statement on standards for attestation engagements no. 2, Reporting on an entity's internal control over financial reporting, Statement on standards for attestation engagements no. 3, Compliance attestation;Amendments to Statement on standards for attestation engagements no. 1, Attestation standards, Statement on standards for attestation engagements no. 2, Reporting on an entity's internal control over financial reporting, Statement on standards for attestation engagements no. 3, Compliance attestation; Exposure draft (American Institute of Certified Public Accountants), 1998, June 1

American Institute of Certified Public Accountants. Auditing Standards Board

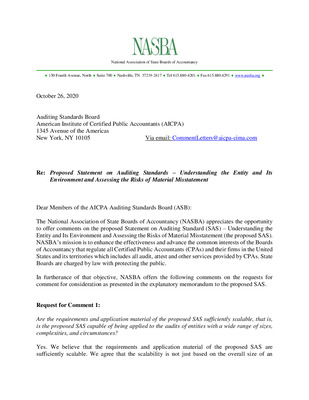

An attestation engagement is one in which a practitioner expresses a conclusion about the reliability of a written assertion or statement that is the responsibility of another party. For example, management may state that the entity's internal control over financial reporting is effective as of a certain date or for a specified period of time. Such engagements are performed pursuant to the Statements on Standards for Attestation Engagements (SSAEs) which are promulgated by the Auditing Standards Board (ASB). The type of subject matter that could be addressed by such assertions is broad and includes internal control, compliance with laws and regulations, or other subject matter that could be useful to a decision maker. [A practitioner's engagement to report on historical financial statements is excluded from the scope of the SSAE as such engagements are addressed by the Statements on Auditing Standards (SASs).] The SSAEs were first issued approximately ten years ago. During the past several years, there has been a proliferation of engagements performed pursuant to the SSAEs. The ASB believes that the demand for attest engagements will continue to grow as decision makers increasingly look to CPAs to to enhance the reliability of information on which decision makers rely, beyond historical financial statements. For example, it is expected that many of the services developed by the Assurance Services Executive Committee of the AICPA will include engagements performed pursuant to the SSAEs. The recently developed Web Trust service, which provides assurance about policies and controls of entities offering services or products for sale over the Internet, is an example of such a service provided pursuant to the SSAEs. Additionally, regulators are increasingly looking to obtain assurance from the public accounting profession as to the reliability of an entity's assertions about internal control, compliance with laws and regulations and a variety of other matters. Finally, the SSAEs allow a great deal of flexibility as to the nature and scope of the engagement and provide the profession with many opportunities to help decision makers satisfy their needs. The ASB has undertaken a series of projects to improve the utility of the SSAEs. This exposure draft is one of a series of anticipated exposure drafts resulting from the ASB's efforts to achieve this objective. In order to improve the utility of the SSAEs, the ASB intends to focus on the needs of the decision makers and to identify improvements that can be made to the SSAEs to best meet those needs. This exposure draft focuses primarily on improving the understandability of the conclusions communicated by the practitioner in an attest engagement. Additionally, by clarifying how the Statements on Quality Control Standards (SQCSs) relate to the SSAEs, the ASB is explicitly recognizing the importance of performing attestation engagements within an appropriate framework to ensure that the public accounting profession's reputation for high quality professional services is perpetuated. This proposed SSAE: 1. Would enable the practitioner to report directly to the client his or her conclusion on a specified subject matter, such as internal control, rather than on management's assertion about internal control. 2. Would eliminate the requirement for a separate presentation of management's assertion in certain cases where the assertion is included in the introductory paragraph of the practitioner's report. 3. Would conform the reporting guidance to include reporting elements similar to those required in auditor reports on historical financial statements as contained in SAS No. 58, Reports on Audited Financial Statements (AICPA, Professional Standards, vol. 1, AU sec. 508). 4. Provides guidance on the relationship between the SSAEs and SQCSs. Enabling direct reporting will require amendments to: a. SSAE No. 1, Attestation Standards (AICPA, Professional Standards, vol. 1, AT sec. 100); b. SSAE No. 2, Reporting on an Entity's Internal Control Over Financial Reporting (AICPA, Professional Standards, vol. 1, AT sec. 400); c. SSAE No. 3, Compliance Attestation (AICPA, Professional Standards, vol. 1, AT sec. 500).

-

, 1998, Dec. 30 by American Institute of Certified Public Accountants. Discount Accretion Task Force and American Institute of Certified Public Accountants. Accounting Standards Executive Committee")

Proposed statement of position : accounting for discounts related to credit quality;Accounting for discounts related to credit quality; Exposure draft (American Institute of Certified Public Accountants), 1998, Dec. 30

American Institute of Certified Public Accountants. Discount Accretion Task Force and American Institute of Certified Public Accountants. Accounting Standards Executive Committee

This proposed Statement of Position (SOP) addresses accounting for differences between contractual and expected future cash flows from an investor's initial investment in certain loans and debt securities (loans) acquired in a transfer when such differences are attributable, at least in part, to credit quality. It includes such loans acquired in purchase business combinations and would apply to all enterprises. The proposed SOP would limit the yield that may be accreted (accretable yield) to the excess of the investor's estimate of undiscounted expected future principal and interest cash flows (expected future cash flows) over the investor's initial investment in the loan. This SOP would require that the excess of contractual cash flows over expected future cash flows (nonaccretable difference) not be recognized as an adjustment of yield, loss accrual, or valuation allowance. The proposed SOP would also prohibit investors from displaying accretable yield and nonaccretable difference in the balance sheet. The proposed SOP would relate subsequent impairment of the loan to the investor's ability to collect all cash flows expected at acquisition. Subsequent increases in expected future cash flows would be recognized prospectively through adjustment of the loan's yield over its remaining life. The provisions of this proposed SOP would be effective for financial statements issued for fiscal years beginning after June 15, 2000.

-

features of defined benefit pension plans : (proposed amendment to the AICPA audit and accounting guide, Audits of employee benefit plans);Accounting for and reporting of 401(h) features of defined benefit pension plans : (proposed amendment to the AICPA audit and accounting guide, Audits of employee benefit plans); Exposure draft (American Institute of Certified Public Accountants), 1998, Sept. 9 by American Institute of Certified Public Accountants. Employee Benefit Plans Committee")

Proposed statement of position : Accounting for and reporting of 401(h) features of defined benefit pension plans : (proposed amendment to the AICPA audit and accounting guide, Audits of employee benefit plans);Accounting for and reporting of 401(h) features of defined benefit pension plans : (proposed amendment to the AICPA audit and accounting guide, Audits of employee benefit plans); Exposure draft (American Institute of Certified Public Accountants), 1998, Sept. 9

American Institute of Certified Public Accountants. Employee Benefit Plans Committee

This proposed Statement of Position (SOP) would amend chapters 2, 3, and 4 of the AICPA Audit and Accounting Guide Audits of Employee Benefit Plans (the Guide) with conforming changes as of May 1, 1998. This proposed SOP specifies the accounting for and disclosure of 401(h) features of defined benefit pension plans, by both defined benefit pension plans and health and welfare benefit plans. The proposed SOP requires: a. Defined benefit pension plans to record assets held in a 401(h) account related to health and welfare plan obligations for retirees as both assets and liabilities on the face of the statement of net assets available for pension benefits in order to arrive at net assets available for pension benefits. b. 401 (h) account assets used to fund health and welfare benefits, and the changes in those assets, to be reported in the financial statements of the health and welfare benefit plan. Benefit obligations related to the 401(h) account are also required to be reflected in the health and welfare plan financial statements. c. Defined benefit pension plans to disclose in the notes to the financial statements the nature of the assets related to the 401(h) account, and the fact that the assets are available only to pay retirees' health benefits. d. Health and welfare benefit plans to disclose in the notes to the financial statements the fact that retiree health benefits are funded partially through a 401 (h) account of the defined benefit pension plan. This proposed SOP is effective for financial statements for plan years beginning after December 15, 1998. Earlier application is encouraged. Accounting changes adopted to conform to the provisions of this proposed SOP shall be made retroactively. Financial statements of prior plan years are required to be restated to comply with the provisions of this proposed SOP only if they are presented together with the financial statements for plan years beginning after December 15, 1998. If accounting changes were necessary to conform to the provisions of this proposed SOP, that fact shall be disclosed when financial statements for the year in which this proposed SOP is first applied are presented either alone or with financial statements of prior years.

-

Reporting on management's assessment pursuant to the life insurance ethical market conduct program of the Insurance Marketplace Standards Association; Statement of position 98-6;

American Institute of Certified Public Accountants. Insurance Companies Committee

-

, 1998, May 20 by American Institute of Certified Public Accountants. Insurance Companies Committee. Deposit Accounting Task Force")

Statement of Position: Deposit Accounting: Accounting for Insurance and Reinsurance Contracts that Do Not Transfer Insurance Risk; Exposure Draft (American Institute of Certified Public Accountants), 1998, May 20

American Institute of Certified Public Accountants. Insurance Companies Committee. Deposit Accounting Task Force

-

, 1998, Sept. 22 by American Institute of Certified Public Accountants. Investment Companies Committee")

Proposed audit and accounting guide : Audits of investment companies;Audits of investment companies; Exposure draft (American Institute of Certified Public Accountants), 1998, Sept. 22

American Institute of Certified Public Accountants. Investment Companies Committee

This Guide has been written with the assumption that readers are proficient in accounting and auditing in general but not necessarily familiar with the investment company industry. Accordingly, the Guide includes extensive investment company industry background and explanatory material. Chapter 1 provides background information and terminology that is intended to help the reader better understand the industry. Chapters 2 through 4 and chapter 8 focus on the major financial statement components that have unique accounting and auditing requirements for investment companies. Chapter 5 focuses on unique accounting, operational, and auditing aspects of complex capital structures of investment companies, including multiple-class funds, master-feeder funds, and funds of funds. Illustrative financial statements are presented for multiple-class funds, master funds, and feeder funds. Chapter 6 focuses on two distinct aspects of taxes for investment companies: financial statements and other matters, and taxation of regulated investment companies. Chapter 7 focuses on financial statement presentation and disclosure requirements of investment companies. Additional disclosures required by the Securities and Exchange Commission (SEC) for registered investment companies and generally accepted accounting principles (GAAP) disclosure requirements are identified. Illustrative financial statements of a typical open-end management investment company are presented. Chapter 9 provides background information and unique matters related to unit investment trusts. This chapter also contains illustrative financial statements for these entities. Chapter 10 provides background, product design, operational, and regulatory information related to separate accounts of life insurance companies. This chapter also describes auditing considerations and contains illustrative financial statements for these entities. Chapter 11 discusses reports on audited financial statements of investment companies, reports on internal control required by the SEC, reports on processing of transactions by transfer agents, reports on examinations of investment performance statistics, and other reports unique to the investment company industry. Numerous report examples are included in this chapter. Chapter 1 2 provides the basis for conclusions for significant new accounting standards.

-

, 1998, Sept. 4 by American Institute of Certified Public Accountants. Life Insurance Audit Guide Task Force")

Proposed Audit and Accounting Guide : Life and health insurance entities;Life and health insurance entities; Exposure draft (American Institute of Certified Public Accountants), 1998, Sept. 4

American Institute of Certified Public Accountants. Life Insurance Audit Guide Task Force

The proposed Guide discusses those aspects of accounting and auditing unique to life and health insurance entities and was developed to assist life and health insurance entities in preparing financial statements in conformity with generally accepted accounting principles (GAAP) and to assist independent auditors in auditing and reporting on those financial statements. In addition, the proposed Guide contains significant discussions of statutory accounting practices (SAP) that includes laws, regulations, and administrative rulings adopted by the various states that govern the operations and reporting requirements of life insurance entities. Because this is a category B GAAP document as defined by SAS 69, The Meaning of Present Fairly in Conformity With Generally Accepted Accounting Principles in the Independent Auditor's Report, the inclusion of descriptions of SAP does not elevate SAP into GAAP. This proposed Guide also incorporates accounting and financial reporting requirements issued by the Financial Accounting Standards Board (FASB) and the AICPA Accounting Standards Executive Committee (AcSEC) since the issuance of the AICPA Industry Audit Guide Audits of Stock Life Insurance Companies through April 1 5, 1 998. Also incorporated in this proposed Guide are new auditing standards issued through April 15, 1998, by the AICPA Auditing Standards Board since the issuance of the pronouncements that this Guide would supersede.

-

Comment Letters Received as of July 21,1998 on Exposure Draft Proposed Revisions to the AICPA Standards for Performing and Reporting on Peer Review

American Institute of Certified Public Accountants. Peer Review Board

-

, 1998, April 20 by American Institute of Certified Public Accountants. Peer Review Board")

Proposed revisions to the AICPA standards for performing and reporting on peer reviews;AICPA standards for performing and reporting on peer reviews;Standards for performing and reporting on peer reviews; Exposure draft (American Institute of Certified Public Accountants), 1998, April 20

American Institute of Certified Public Accountants. Peer Review Board

The AICPA Peer Review Board is issuing this exposure draft to update the Standards for Performing and Reporting on Peer Reviews (AICPA, Professional Standards, vol. 2, PR sec. 100). This proposal: 1. Expands the definition of an accounting and auditing practice for the purposes of performing and reporting on a peer review to conform with Statement on Quality Control Standards (SQCS) No. 2, System of Quality Control for a CPA Firm's Accounting and Auditing Practice (AICPA Professional Standards, vol. 1, QC sec. 20), thereby including all engagements performed under the Statements on Standards for Attestation Engagements. 2. States that any engagement performed under the Statements on Auditing Standards (SAS) will require an on-site peer review, not just audits of historical financial statements and SAS No. 75, Engagements to Apply Agreed-Upon Procedures to Specified Elements, Accounts, or Items of a Financial Statement (AICPA, Professional Standards, vol. 1, AU sec. 622) engagements to make the standards all inclusive. 3. Replaces the term "owner" with "partner" throughout the peer review standards and adds a footnote defining the term "partner" upon its first use. 4. Replaces the terms "unqualified" and "qualified," which are used to describe the type of peer review report issued with the terms "unmodified" and "modified," respectively. 5. Incorporates Peer Review Standards Interpretation No. 4, "Reviewer Requirements" into the body of the peer review standards. 6. Clarifies that attest engagements should be subject to selection if the date of the report for the engagement falls within the year to be reviewed. 7. Revises the standard language used in the peer review report and letter of comments to make them more easily read and understood by all users. The proposed changes will be incorporated into the AICPA Standards for Performing and Reporting on Peer Reviews effective for peer reviews that commence on or after January 1, 1999. Early implementation is encouraged.

-

, 1998, April 15 by American Institute of Certified Public Accountants. Professional Ethics Executive Committee")

Omnibus proposal of Professional Ethics Division interpretations and rulings; Exposure draft (American Institute of Certified Public Accountants), 1998, April 15

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

1. PROPOSED REVISION OF THE DEFINITION OF CLIENT UNDER ET SECTION 92; 2. PROPOSED REVISION OF INTERPRETATION 101-2 UNDER RULE 101: Former Practitioners and Firm Independence; 3. PROPOSED REVISION OF RULING NO. 191 UNDER RULE 501 AND RULING NO. 22 UNDER RULE 301: Member Removing Client Files From an Accounting Firm; 4. PROPOSED INTERPRETATION UNDER RULE 101: The Effect of Alternative Practice Structures on the Applicability of Independence Rules; 5. PROPOSED REVISION OF ET SECTION 91.02, Applicability; 6. PROPOSED REVISION OF INTERPRETATION 505-2 UNDER RULE 505: Application of Rules of Conduct to Members Who Operate Own a Separate Business; 7. PROPOSED INTERPRETATION UNDER RULE 505: Application of Rule 505 to Alternative Practice Structures.

-

, 1998, Nov. 16 by American Institute of Certified Public Accountants. Professional Ethics Executive Committee")

Omnibus proposal of Professional Ethics Division interpretations and rulings; Exposure draft (American Institute of Certified Public Accountants), 1998, Nov. 16

American Institute of Certified Public Accountants. Professional Ethics Executive Committee

1. PROPOSED REVISION OF INTERPRETATION 101-3 UNDER RULE 101: Provision of Other Accounting Services to Clients; 2. PROPOSED RULING UNDER RULE 101 AND RULE 102: Member Is Connected With an Entity That Has a Loan to a Client; 3. PROPOSED REVISION OF INTERPRETATION 102-1 UNDER RULE 102: Knowing Misrepresentations in the Preparation of Financial Statements or Records; 4. PROPOSED RULING UNDER RULE 302: Investment Advisory Services; 5. PROPOSED RULING UNDER RULE 302 AND RULE 503: Commission and Contingent Fee Arrangements With Nonattest Client; 6. PROPOSED REVISION OF INTERPRETATION 501-4 UNDER RULE 501: Negligence in the Preparation of Financial Statements or Records; 7. PROPOSED INTERPRETATION UNDER RULE 501: Failure to File Tax Return or Pay Tax Liability; 8. PROPOSED DELETION OF INTERPRETATION 505-1 UNDER RULE 505: Investment in Accounting Organization

-

Engagements to perform year 2000 agreed-upon procedures attestation engagements pursuant to rule 17a-5 of the Securities Exchange Act of 1934, rule 17Ad-18 of the Securities Exchange Act of 1934, and advisories no. 17-98 and no. 40-98 of the Commodity Futures Trading Commission; Statement of position 98-8;

American Institute of Certified Public Accountants. Securities Industry Year 2000 Agreed-Upon Procedures Task Force

-

Audits of states, local governments, and not-for-profit organizations receiving federal awards; Statement of position 98-3;

American Institute of Certified Public Accountants. Single Audit Working Group

-

Comment Letters to proposed statement on standards for attestation engagements : Management's discussion and analysis;

American Institute of Certified Public Accountants. Accounting Standards Board

-

Accounting by insurance and other enterprises for insurance-related assessments; Statement of position 97-3;

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

Accounting by participating mortgage loan borrowers; Statement of position 97-1;

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

Comment letter on Accounting for derivative and similar financial instruments and for hedging activities

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

Comment Letter on the FASB’s June 11, 1997 Exposure Draft of a Proposed Statement of Financial Accounting Concepts, Using Cash Flow Information in Accounting Measurements.

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

Comment letters on Employers' disclosures about pensions and other postretirement benefits : an amendment of FASB statements no. 87, 88, and 106

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

![Comment Letters on IASC Exposure Drafts, Entitled: [1] Interim Financial Reporting (E57) [2] Discontinuing Operations (E58) [3] Provisions, Contingent Liabilities and Contingent Assets (E59) [4] Intangible Assets (E60) [5] Business Combinations (E61). by American Institute of Certified Public Accountants. Accounting Standards Executive Committee](https://egrove.olemiss.edu/aicpa_sop/2131/thumbnail.jpg "Comment Letters on IASC Exposure Drafts, Entitled: [1] Interim Financial Reporting (E57) [2] Discontinuing Operations (E58) [3] Provisions, Contingent Liabilities and Contingent Assets (E59) [4] Intangible Assets (E60) [5] Business Combinations (E61). by American Institute of Certified Public Accountants. Accounting Standards Executive Committee")

Comment Letters on IASC Exposure Drafts, Entitled: [1] Interim Financial Reporting (E57) [2] Discontinuing Operations (E58) [3] Provisions, Contingent Liabilities and Contingent Assets (E59) [4] Intangible Assets (E60) [5] Business Combinations (E61).

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

Comment Letters to proposed statement of position: reporting on the costs of start-up activities;

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

Comment Letters to proposed statement on auditing standards and statement on standards for attestation engagements : establishing an understanding with the client;

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

Comment Letters to Proposed Statement on Auditing Standards, Communication between predecessor and successor auditors;

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

Comment letters to proposed statement on auditing standards: Management representations;

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

, 1997, June 30 by American Institute of Certified Public Accountants. Accounting Standards Executive Committee")

Proposed statement of position : deposit accounting : accounting for insurance and reinsurance contracts that do not transfer insurance risk;Deposit accounting : accounting for insurance and reinsurance contracts that do not transfer insurance risk; Exposure draft (American Institute of Certified Public Accountants), 1997, June 30

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

This proposed Statement of Position (SOP) provides guidance on how to account for insurance and reinsurance contracts that do not transfer insurance risk. It applies to all entities and all insurance and reinsurance contracts that do not transfer insurance risk except for long-duration life and health insurance contracts. The method used to account for insurance and reinsurance contracts that do not transfer insurance risk is referred to in this proposed SOP as deposit accounting. The proposed SOP does not address when deposit accounting should be applied. This proposed SOP specifies the following: 1. Insurance and reinsurance contracts for which the deposit method is appropriate should be classified as one of the following, which are those: a. That transfer only significant timing risk. b. That transfer only significant underwriting risk. c. That transfer neither significant timing nor underwriting risk. d. With indeterminate risk. 2. At inception, a deposit asset or liability should be recognized for insurance and reinsurance contracts accounted for under deposit accounting and should be measured based on the consideration paid or received less any explicitly identified premiums or fees to be retained by the insurer or reinsurer. 3. Insurance and reinsurance contracts that transfer neither significant timing nor underwriting risk and insurance and reinsurance contracts that transfer only significant timing risk should be accounted for using the interest method. Changes in estimates of the timing or amounts of recoveries should be accounted for by recalculating the effective yield. The asset or liability should then be adjusted to the amount that would have existed had the new effective yield been applied since the inception of the contract. The revenue and expense recorded for such contracts shall be included in interest income or interest expense. 4. Insurance or reinsurance contracts that transfer only significant underwriting risk should be accounted for by measuring the deposit based on the unexpired portion of the coverage provided until losses are incurred that will be reimbursed under the contracts. Once a loss is incurred that will be reimbursed under this kind of contract, the deposit should be measured by the present value of the expected future cash flows arising from the contract plus the remaining unexpired portion of the coverage provided. Changes in the recorded amount of the deposit, other than the unexpired portion of the coverage provided, should be included in the income statement of the insured as an offset against the loss recorded by the insured that will be reimbursed under the contract and in an insurer's income statement as an incurred loss. The reduction in the deposit related to the unexpired portion of the coverage provided should be recorded by the insured and the insurer who are insurance enterprises as an adjustment to incurred losses. If the insured and the insurer are enterprises other than insurance enterprises, the reduction in the deposit related to the unexpired portion of the coverage provided should be recorded as an expense. 5. For insurance and reinsurance contracts with indeterminate risk, the guidance in SOP 92-5, Accounting for Foreign Property and Liability Reinsurance, as to the open-year method, should be followed. The open-year method should not, however, be used to defer losses that otherwise would be recognized pursuant to FASB Statement No. 5. Under the open-year method, the effects of the contracts are not included in the determination of net income until sufficient information becomes available to reasonably estimate and allocate premiums. The open-year method requires that these effects be aggregated in the balance sheet. When sufficient information becomes available to reasonably estimate and allocate premiums, the insurance or reinsurance contract with indeterminate risk should be reclassified into one of the other three categories as an insurance or reinsurance contract that transfers neither significant timing nor underwriting risk, transfers only significant timing risk, or transfers only significant underwriting risk, as appropriate, and accounted for accordingly. This proposed SOP is effective for financial statements for fiscal years beginning after December 15, 1998, with earlier adoption encouraged. Restatement of previously issued annual financial statements would not be permitted. Initial application of this proposed SOP should be as of the beginning of an entity's fiscal year (that is, if the proposed SOP were adopted before the effective date and during an interim period, all prior interim periods would be required to be restated). The effect of initially adopting this SOP should be reported as a cumulative effect of a change in accounting principle (in accordance with the provisions of Accounting Principles Board Opinion No. 20, Accounting Changes).

-

1997, February 11 by American Institute of Certified Public Accountants. Accounting Standards Executive Committee")

Proposed Statement of Position: Reporting on the Costs of Start-up Activities, Draft - Not for Public Distribution, February 11, 1997; Exposure Draft (American Institute of Certified Public Accountants) 1997, February 11

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

, 1997, Apr. 22 by American Institute of Certified Public Accountants. Accounting Standards Executive Committee")

Proposed statement of position : Reporting on the costs of start-up activities;Reporting on the costs of start-up activities; Exposure draft (American Institute of Certified Public Accountants), 1997, Apr. 22

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

This Statement of Position (SOP) provides guidance on the financial reporting of start-up costs. It requires costs of start-up activities to be expensed as incurred. The SOP broadly defines start-up activities and provides examples to help entities determine what costs are and are not within the scope of this SOP. This SOP applies to all nongovernmental entities and is effective for financial statements for fiscal years beginning after December 15, 1997. Earlier application is encouraged in fiscal years for which financial statements previously have not been issued.

-

; 1997, June 5 by American Institute of Certified Public Accountants. Accounting Standards Executive Committee")

Proposed statement of position : Software revenue recognition, Draft - 6/5/97; Exposure draft (American Institute of Certified Public Accountants); 1997, June 5

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

Software revenue recognition; Statement of position 97-2;

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

Statement of Position: Accounting for the Costs of Computer Software Developed or Obtained for Internal Use, November 17, 1997, Draft - For Discussion Only

American Institute of Certified Public Accountants. Accounting Standards Executive Committee

-

")

Comment letters on proposed the SOP on Deposit Accounting, 3162.DA

American Institute of Certified Public Accountants (AICPA)

-

, 1997, November 24 by American Institute of Certified Public Accountants. Auditing Standards Board")

Proposed auditing interpretation : the use of legal interpretations as evidential matter to support management's assertion that a transfer of financial assets qualifies as a sale; Exposure draft (American Institute of Certified Public Accountants), 1997, November 24

American Institute of Certified Public Accountants. Auditing Standards Board

-

;Proposed statement on standards for attestation engagements : establishing an understanding with the client : (amendments to Statement on auditing standards no. 1, AU section 310, \"Relationship between the auditor's appointment and planning\" and Statement on standards for attestation engagements no. 1, AT section 100, \"Attestation standards\") ;Establishing an understanding with the client : (amendments to Statement on auditing standards no. 1, AU section 310, \"Relationship between the auditor's appointment and planning\" and Statement on standards for attestation engagements no. 1, AT section 100, \"Attestation standards\"); Exposure draft (American Institute of Certified Public Accountants), 1997, Mar. 7 by American Institute of Certified Public Accountants. Auditing Standards Board")

Proposed statement on auditing standards and statement on standards for attestation engagements : establishing an understanding with the client : (amendments to Statement on auditing standards no. 1, AU section 310, "Relationship between the auditor's appointment and planning" and Statement on standards for attestation engagements no. 1, AT section 100, "Attestation standards") ;Proposed statement on standards for attestation engagements : establishing an understanding with the client : (amendments to Statement on auditing standards no. 1, AU section 310, "Relationship between the auditor's appointment and planning" and Statement on standards for attestation engagements no. 1, AT section 100, "Attestation standards") ;Establishing an understanding with the client : (amendments to Statement on auditing standards no. 1, AU section 310, "Relationship between the auditor's appointment and planning" and Statement on standards for attestation engagements no. 1, AT section 100, "Attestation standards"); Exposure draft (American Institute of Certified Public Accountants), 1997, Mar. 7

American Institute of Certified Public Accountants. Auditing Standards Board

The Auditing Standards Board (ASB) is proposing an amendment to existing standards to provide guidance on obtaining an understanding with the client about the services to be performed. Currently, such guidance is not included in the Statements on Auditing Standards (SASs) or the Statements on Standards for Attestation Engagements (SSAEs). However, the recently-issued Statement on Quality Control Standards (SQCS) No. 2, System of Quality Control for a CPA Firm's Accounting and Auditing Practice, (AICPA, Professional Standards, vol. 2, QC sec.20) requires that a CPA firm provide policies and procedures for obtaining an understanding with the client regarding services to be performed. SQCS No. 2 also states that professional standards may provide guidance in deciding whether such understanding should be oral or written. The ASB recognizes a need for authoritative guidance about this issue to reduce misunderstandings as to the nature of the audit and attest engagement to be performed. The proposed Statements would amend existing professional standards to incorporate guidance about obtaining an understanding with the client regarding the services to be performed. The proposed Statements would require the auditor to establish an understanding with the client that includes the objectives of the engagement, the responsibilities of management and the auditor, and any limitations of the engagement. The proposed Statements also would require that the auditor document his or her understanding with the client in the working papers, preferably through a written communication with the client. The proposed Statements would include specific matters that ordinarily would be addressed in the understanding with the client. In addition, the proposed Statements would provide guidance when the auditor believes that an understanding with the client has not been established. The proposed Statements would amend: 1. SAS No. 1, Codification of Auditing Standards and Procedures (AICPA, Professional Standards, vol. 1, AU sec. 310), and would change the title of the section from "Relationship Between the Auditor's Appointment and Planning" to "Appointment of the Independent Auditor." 2. SSAE No. 1, Attestation Standards (AICPA, Professional Standards, vol. 1, AT sec. 100).

-

;Communications between predecessor and successor auditors : (to supersede Statement on auditing standards no. 7, Communications between predecessor and successor auditors, and its interpretations); Exposure draft (American Institute of Certified Public Accountants), 1997, Mar. 7 by American Institute of Certified Public Accountants. Auditing Standards Board")

Proposed statement on auditing standards : communications between predecessor and successor auditors : (to supersede Statement on auditing standards no. 7, Communications between predecessor and successor auditors, and its interpretations);Communications between predecessor and successor auditors : (to supersede Statement on auditing standards no. 7, Communications between predecessor and successor auditors, and its interpretations); Exposure draft (American Institute of Certified Public Accountants), 1997, Mar. 7

American Institute of Certified Public Accountants. Auditing Standards Board

The Auditing Standards Board (ASB) has issued this exposure draft to provide appropriate guidance on the auditor's responsibility regarding communications between predecessor and successor auditors. This proposed Statement provides guidance relating to communications between predecessor and successor auditors when a change of auditors has taken place or is in process. This proposed Statement: 1. Revises the definitions of predecessor and successor auditors to reflect the current proposal environment found in today's practice. 2. Expands the required communications with the predecessor auditor before the successor auditor accepts an engagement to include inquiries about communications made by the predecessor auditor to audit committees or others with equivalent authority and responsibility as described in SAS No. 82, Consideration of Fraud in a Financial Statement Audit (AICPA, Professional Standards, vol. 1, AU sec. 316), SAS No. 54, Illegal Acts by Clients (AICPA, Professional Standards, vol. 1, AU sec. 317), and SAS No. 60, Communication of Internal Control Related Matters Noted in an Audit (AICPA, Professional Standards, vol. 1, AU sec. 325), and any other reasonable inquiries that the successor auditor may wish to ask the predecessor auditor. 3. Clarifies the successor auditor's responsibility with respect to obtaining sufficient competent evidential matter used in analyzing the impact of the opening balances on the current year financial statements and consistency of accounting principles as a matter of professional judgment. Examples of audit evidence provided include the most recent audited financial statements, the predecessor auditor's report thereon, the results of inquiry of the predecessor auditor, the results of the successor auditor's review of the predecessor auditor's working papers, and audit procedures performed on the current period's transactions that may provide evidence about the opening balances or consistency. 4. Expands the working papers ordinarily made available to the successor auditor by the predecessor auditor to include documentation of planning, internal control, audit results and other matters of continuing audit significance. 5. Introduces an illustrative client consent and acknowledgment letter and an illustrative successor auditor acknowledgment letter. A predecessor auditor may conclude that obtaining written communications from both the former client and the successor auditor will allow greater communication between both parties and greater access to the working papers than would be the case in the absence of such communications. The ASB believes that it is in the public interest for successor auditors to have greater access to working papers and, accordingly, for all practitioners to have access to these letters and to use them in their practice if they so choose. These letters are presented for illustrative purposes only and not as a requirement by the proposed Standard. 6. Incorporates the Interpretations, Communications Between Predecessor and Successor Auditors Auditing Interpretations of Section 315 (AICPA, Professional Standards, vol. 1, AU sec. 9315), into the proposed Statement. This proposed Statement would supersede SAS No. 7, Communications Between Predecessor and Successor Auditors (AICPA, Professional Standards, vol. 1, AU sec. 315), and Its Interpretations.

-

and an amendment to Statement on auditing standards no. 58, Reports on audited financial statements;Management representations (to supersede Statement on auditing standards no. 19, Client representations, and Auditing interpretation no. 2 \"Management representations when current management was not present during the period under audit\") and an amendment to Statement on auditing standards no. 58, Reports on audited financial statements; Exposure draft (American Institute of Certified Public Accountants), 1997, June 9 by American Institute of Certified Public Accountants. Auditing Standards Board")

Proposed Statement on auditing standards : Management representations (to supersede Statement on auditing standards no. 19, Client representations, and Auditing interpretation no. 2 "Management representations when current management was not present during the period under audit") and an amendment to Statement on auditing standards no. 58, Reports on audited financial statements;Management representations (to supersede Statement on auditing standards no. 19, Client representations, and Auditing interpretation no. 2 "Management representations when current management was not present during the period under audit") and an amendment to Statement on auditing standards no. 58, Reports on audited financial statements; Exposure draft (American Institute of Certified Public Accountants), 1997, June 9

American Institute of Certified Public Accountants. Auditing Standards Board

The Auditing Standards Board (ASB) has issued this exposure draft to provide appropriate guidance regarding written management representations to be obtained by an auditor as part of an audit performed in accordance with generally accepted auditing standards. A task force of the ASB reviewed Statement on Auditing Standards (SAS) No. 19, Client Representations (AICPA, Professional Standards, AU sec. 333), and determined that it needed to be updated to reflect changes in auditing practice and the auditing environment since SAS No. 19 was issued. This proposed Statement would supersede SAS No. 19. This proposed Statement: 1. Clarifies the requirement for an auditor to obtain written representations for all financial statements and periods covered by the auditor's report. 2. Includes a representation made by management that states that it is management's belief that the financial statements are fairly presented in conformity with generally accepted accounting principles. 3. Includes a list of updated specific representations to be obtained from management that are consistent with representations obtained in current practice. Such representations include information concerning fraud as referred to in SAS No. 82, Consideration of Fraud in a Financial Statement Audit (AICPA, Professional Standards, vol. 1, AU sec. 316) and significant estimates and material concentrations known to management that are required to be disclosed in accordance with the AlCPA's Statement of Position 94-6, Disclosure of Certain Significant Risks and Uncertainties. 4. States that the auditor ordinarily should obtain a representation letter tailored to cover representations relating to the financial statements unique to the entity's business or industry. Also, appendix B, "Additional Representations," has been added to the proposed Statement and includes additional representations that may be appropriate in certain situations. 5. Requires the auditor to investigate the circumstances and consider the reliability of a representation made, if that representation is contradicted by other audit evidence. 6. Includes guidance regarding materiality levels that may be stated explicitly in the representation letter, in either qualitative or quantitative terms. Also, the illustrative management representation letter included in appendix A, "Illustrative Management Representation Letter," includes a aulatiative discussion of materiality. 7. Includes guidance for circumstances when an auditor should obtain an updated representation letter from management such as when a predecessor auditor is requested by a former client to reissue his or her report on the financial statements of a prior period. Also, an illustrative updating management representation letter has been added to the proposed Statement in appendix C, "Illustrative Updating Management Representation Letter." This exposure draft contains a proposed revision to SAS No. 58, Reports on Audited Financial Statements (AICPA, Professional Standards, vol 1, AU sec. 508.71), which would expand a predecessor auditor's procedures when asked by a former client to reissue his or her report on the financial statements of a prior period. This proposed amendment would require the predecessor auditor to obtain a letter of representation from management, in addition to the representation letter from the successor auditor, before reissuing a report previously issued on financial statements of a prior period. See the section herein entitled, "Proposed Amendment to Statement on Auditing Standards No. 58, Reports on Audited Financial Statements." In conjunction with the proposed amendment to SAS No. 58, an illustrative updating management representation letter is included as appendix C, "Illustrative Updating Management Representation Letter," of the proposed Statement. This proposed Statement would supersede SAS No. 19 and Auditing Interpretation No. 2, "Management Representations When Current Management Was Not Present During the Period Under Audit" (AICPA, Professional Standards, vol. 1, AU sec. 9333). It also would amend SAS No. 58.

-

, 1997, Mar. 7 by American Institute of Certified Public Accountants. Auditing Standards Board")

Proposed statement on standards for attestation engagements : management's discussion and analysis ;Management's discussion and analysis; Exposure draft (American Institute of Certified Public Accountants), 1997, Mar. 7

American Institute of Certified Public Accountants. Auditing Standards Board

The Auditing Standards Board (ASB) is considering the issuance of a Statement on Standards for Attestation Engagements (SSAE) to provide guidance to practitioners who may be engaged to examine or review management's discussion and analysis (MD&A) prepared pursuant to the published rules and regulations of the Securities and Exchange Commission (SEC). The ASB has observed the following since a proposed SSAE was first issued for exposure in 1987, and subsequently deferred: 1. Possible changes may occur in the existing financial reporting model as a result of the Comprehensive Model for Business Reporting proposed by the AICPA Special Committee on Financial Reporting. Such model is more forward-looking than the current financial reporting model; management's discussion and analysis that public registrants are currently required to prepare addresses certain elements proposed by the model. 2. During the research performed by the AICPA Special Committee on Financial Reporting, some users expressed a desire for more auditor involvement in financial information that they receive. 3. Existing guidance does not address a number of issues practitioners should consider in applying the Attestation Standards to an engagement to examine or review MD&A (including whether the practitioner needs to have audited or reviewed the financial statements to which the MD&A relates; internal control considerations; application of materiality considerations in the performance of an examination and in forming an opinion on, or providing the basis for reporting on a review of, the MD&A presentation; and the nature of specific procedures that should be performed), whether a review level of service is appropriate for MD&A, or whether it is appropriate to accept an engagement with respect to a presentation similar to MD&A in a non-SEC environment. Accordingly, the ASB believes that the profession should be proactive rather than reactive to changes in the business environment and be appropriately positioned to provide such service if requested. The ASB also believes that the proposed Standard would provide a framework that may be useful in providing assurance services in the future as companies experiment with new forms of financial presentations, such as the Comprehensive Model for Business Reporting. An examination or a review of MD&A would provide a higher level of assurance as to reasonableness to both the users and the preparers of the MD&A than is provided today in the context of an audit of financial statements. Existing standards included in Statement on Auditing Standards (SAS) No. 8, Other Information in Documents Containing Audited Financial Statements (AICPA, Professional Standards, vol. 1, AU sec. 550), only require the auditor to read the MD&A and consider whether the MD&A, or the manner of its presentation, is materially inconsistent with information, or the manner of its presentation, appearing in the financial statements. A comparison of the procedures under SAS No. 8 versus an examination or review of MD&A appears in the Table at the end of this Summary. An examination of MD&A would provide both the users and the preparers with an independent opinion regarding whether the presentation includes the required elements of Item 303 of Regulation S-K and the related published SEC rules and regulations, whether the historical financial information included in the MD&A is accurately derived from the entity's financial statements, and whether the underlying information and assumptions of the entity provide a reasonable basis for the disclosures contained therein. A review of MD&A would provide users and preparers with negative assurance concerning such matters. In addition to the assurance that is obtained from an examination or a review level of service, management would also benefit by improving the MD&A through an independent view of the content. Improvements to the MD&A presentation improve the quality of information available to users. Audit committees might benefit through the additional discussions with the auditors and review of the draft MD&A presentation that would result from an examination or review engagement. This proposed Statement provides guidance to assist the practitioner in the following: 1. Accepting an engagement; 2. Planning the engagement; 3. Considering internal control applicable to the preparation of MD&A; 4. Obtaining sufficient evidence for an examination; 5. Applying analytical procedures and inquiries for a review; 6. Considering events subsequent to the balance-sheet date; 7. Reporting. Fundamental to accepting an engagement to examine MD&A under this proposed Statement is the requirement for the practitioner to have audited the financial statements for at least the latest period subject to his or her examination of MD&A. Similarly, in order to accept an engagement to review MD&A, the practitioner is required to have performed either an audit of the annual financial statements or a review of interim financial statements for at least the latest period to which the MD&A presentation relates. If there is a predecessor practitioner who examined or reviewed the MD&A for a prior period(s), the successor practitioner may refer to the reports of the predecessor practitioner for the earlier period(s) if the predecessor practitioner's permission is obtained. Otherwise, the successor practitioner is required to apply the appropriate procedures relating to information concerning prior years included in the current MD&A presentation in order to examine or review such prese d36 ntation. If the practitioner is requested by entities to provide this service, the proposed Statement would be applied to engagements by public companies that are required to follow Item 303 of Regulation S-K and nonpublic entities that choose to prepare MD&A using the published SEC rules and regulations. Although an engagement to perform an examination or review of an MD&A presentation may be performed under SSAE No. 1, Attestation Standards, this proposed Statement expands on the guidance in such standard by providing specific guidance with respect to engagement acceptance, performance issues, and reporting matters for an MD&A presentation. SAS No. 8, which requires the auditor to read the MD&A and consider whether the MD&A or its presentation is materially inconsistent with information, or the manner of its presentation, appearing in the financial statements, would continue to apply to situations in which the auditor is not engaged to examine or review the MD&A presentation. This proposed SSAE would require amending various paragraphs of SAS No. 72, Letters for Underwriters and Certain Other Requesting Parties (AICPA, Professional Standards, vol. 1, AU sec. 634), to permit accountants to examine or review and report separately on an Item 303 MD&A presentation. Accordingly, the proposed amendments to SAS No. 72 are included as an appendix to this proposed SSAE. Commentators to this proposed Statement should be aware that practitioners performing an engagement to examine or review MD&A under this proposed Statement must be independent pursuant to rule 101 of the Code of Professional Conduct (AICPA, Professional Standards, vol. 2, ET sec. 101) because of the required condition that the practitioner has to have audited or reviewed historical financial statements for at least the latest period to which the MD&A presentation applies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}